How Corporate Accounting Teams Use machine grade audit trails to replace the traditional annual financial close

As a result, companies can finalize all of their financial transactions without any lengthy descriptions being required months later.

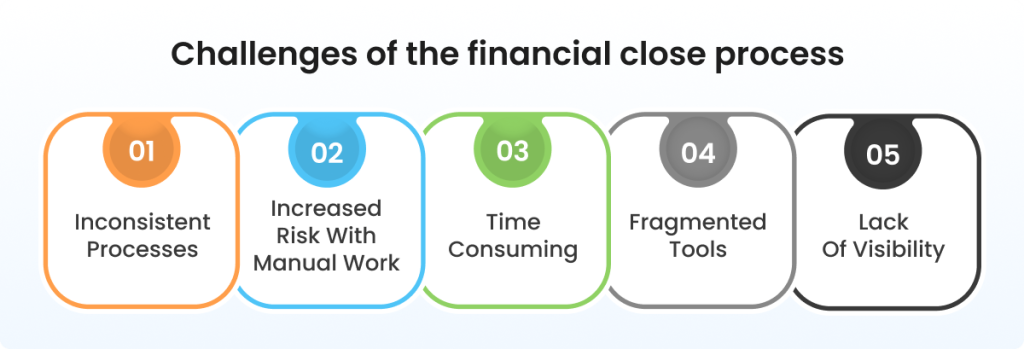

Why the annual close is losing ground

While the year-end close remains important for statutory reporting for companies that follow generally accepted accounting principles (GAAP) and IFRS, it is no longer the only way finance departments want to obtain visibility into their financial status. With the increased desire of finance departments to produce real-time data, the pressure is on for finance teams to perform at a faster pace, with fewer mistakes, and provide clean numbers to management all year long rather than waiting until after a lengthy reconciliation process.

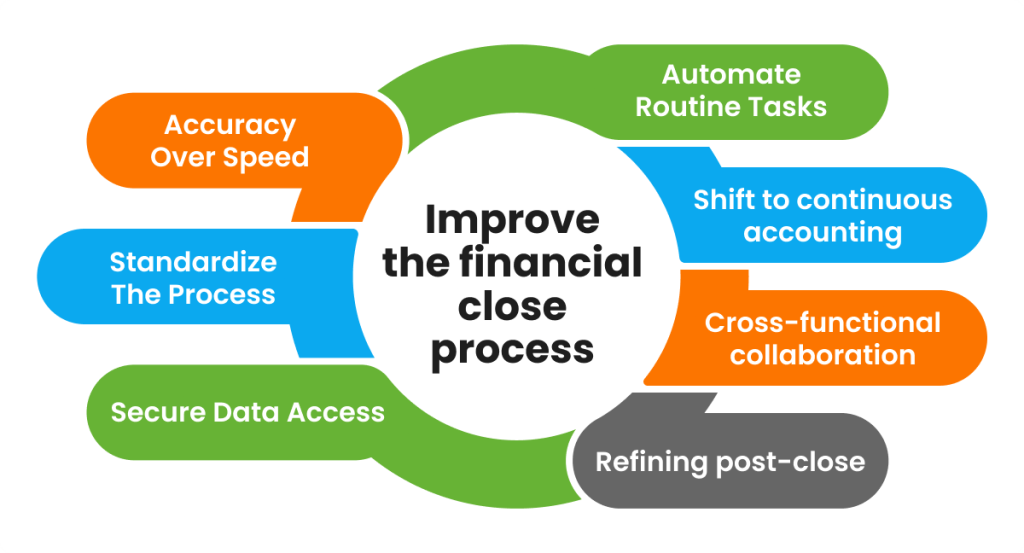

This is where financial close automation will play a vital role in helping finance departments achieve this objective. By moving away from considering the close as a single event that occurs once per year, and instead focusing on developing an ongoing record of activity from which final balances can be confirmed anytime during the year, accounting departments can reduce the number of surprises at the time of the year-end close process; decrease the number of manual adjustments; and greatly reduce reliance on 'heroic' use of spreadsheets.

What machine-grade audit trails actually do

Fundamentally, an audit trail is a sequential log of activities performed by individuals—who did what, when, and why. In accounting, the audit trail consists of, but not limited to, supporting documents (called source documents), general ledger entries, all forms of approvals, modifications, system activity, and the data’s movement from the initial transaction through to the final financial statement prepared from the data.

The term “machine grade” refers to the degree of exactness, timeliness, and traceability of information contained in the audit trail, allowing a reviewer to produce the complete financial picture (from the initial transaction through to the final financial statement) without relying on memory or the need for manual review. This is especially beneficial when an organisation has a large volume of transactions, or when several organisations are involved in the transaction with each using different currencies, and/or accounting systems.

Why this matters for finance teams

Accounting leaders see the value in accounting not merely as a means of meeting compliance requirements, but as a way of controlling the accounting process. By having the ability to track changes made to the accounting records along with supporting documentation related to the changes, accounting teams are able to identify irregularities sooner than they would have otherwise, investigate exceptions with less friction than they would have experienced otherwise, and lessen the level of anxiety that typically builds at the end of an accounting period.

Additionally, by utilizing a centralized and time-stamped accounting record, accounting teams lower the number of version control disputes and "where did this number come from?" discussions. This is important because, in the real world, finance teams need their numbers to be balanced, but they also need to be able to defend them.

How the close process changes

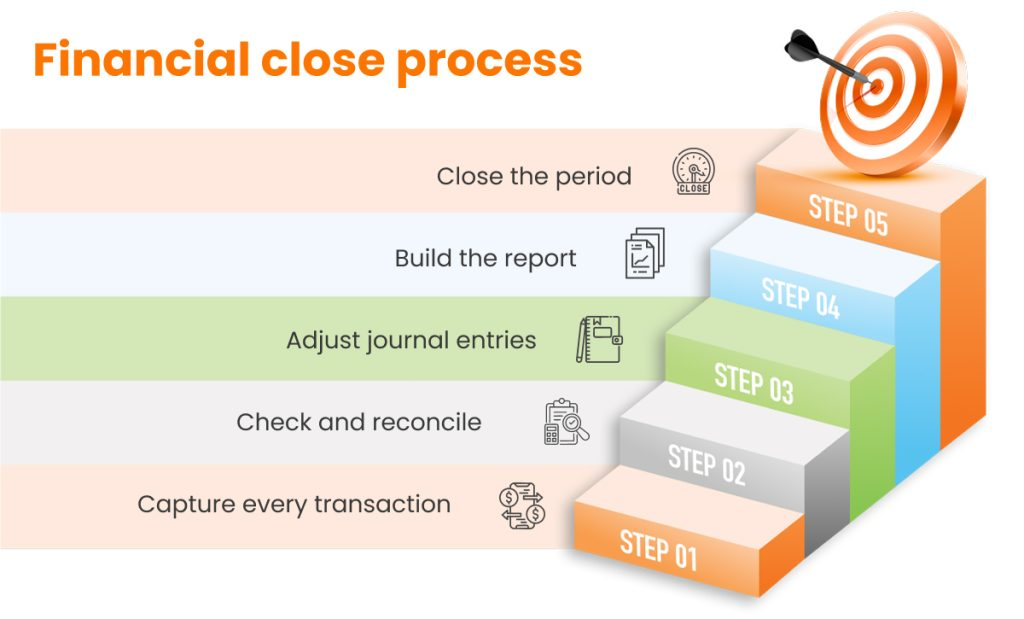

Traditional closings have been based on the process of gathering data from multiple locations (batching), reconciling the data, making the necessary adjustments, and then repeating this process up to 12 times per year. The implementation of machine-generated audit trails allows for the implementation of a continuous close where the verification of transactions occurs at the time transactions occur and exceptions are identified sooner. This results in a reduction of the workload at the end of a month or year and the close becomes more of a verification of what has occurred than a rescue effort.

The change to a continuous close does not eliminate the close from the process. The role of accountants changes because the majority of the work performed during the close will be shifted earlier in the process. Instead of spending the final days of the month or year looking for missing or incorrect supporting documents, accountants will be able to spend more time reviewing real-time information, refining controls, and addressing the few remaining items that are subject to interpretation.

The tech behind the shift

The larger story of digital transformation in accounting includes cloud-based systems, automated processes, AI-enabled workflow processes, and centralized storage systems. These tools provide a complete audit trail by instead of having invoicing, approval, bank information, reconciliation and reporting kept separately in file cabinets or email threads, they give you all of this information as one smooth flow.

When data is all in one controlled location, it is much easier to have faith in the audit trail and to review the audit trail. In addition, this allows external auditors and internal reviewers to follow the same evidence chain without requiring the reconstruction of half of the department’s memory from scratch.

The business case is stronger than ever

There is a great deal of interest in adopting machine-sustainable audit trails because of their ability to yield tangible benefits. Decision-making becomes easier with quicker close periods; records become cleaner, thereby reducing the risk of non-compliance; and greater levels of transparency reduce the likelihood of costly surprises. All of these factors can lead to a stronger ability to forecast accurately, create strong controls over financial reporting, and develop an overall finance function that spends less time on the aftermath of month-end-close activity and more time analysing financial results.

Another area that may be overlooked is the human element of automating routine reconciliation tasks and embedding an audit trail through the process. This allows for finance teams to transition away from repetitive, manual tasks to more judgement-based work. Doing so can enhance morale since the level of burnout tends to increase dramatically during the close process.

The major conclusion is this: implementing machine-led audit trails creates not just faster closures, but also new opportunities to improve existing closing processes. Furthermore, the finance organisations that successfully implement machine-assisted audits will have very different financial operations; they will be much more continual, much more accountable, and less reliant on frantic end-of-the-year closings than before.

Latest Posts